Inflation has been and will continue to be a buzzword, but what is it? Inflation is a decrease in the purchasing power of money, reflected in a general increase in the price of goods and services in the economy.

Because the United States is no longer on the gold standard, current monetary policies allow for artificially increasing the money supply, subsequently pushing interest rates near zero. From 2020 to 2021, the US money supply increased by 27% in an effort to ease the recession caused by the pandemic. “To put that in perspective, that is the biggest jump in the money supply in America’s history. That is bigger than the Financial Crisis of 2007-2008 (10%), bigger than World War II (18%), and bigger than FDR’s stimulus to fight the Great Depression (10%).” As the money supply increases, its purchasing power then decreases, causing inflation. But how does the money supply actually increase? Well, there are a few different ways.

Quantitative easing occurs when the central bank purchases long-term securities from the open market. This increases the money supply and encourages investing and lending. Additionally, it also lowers interest rates.

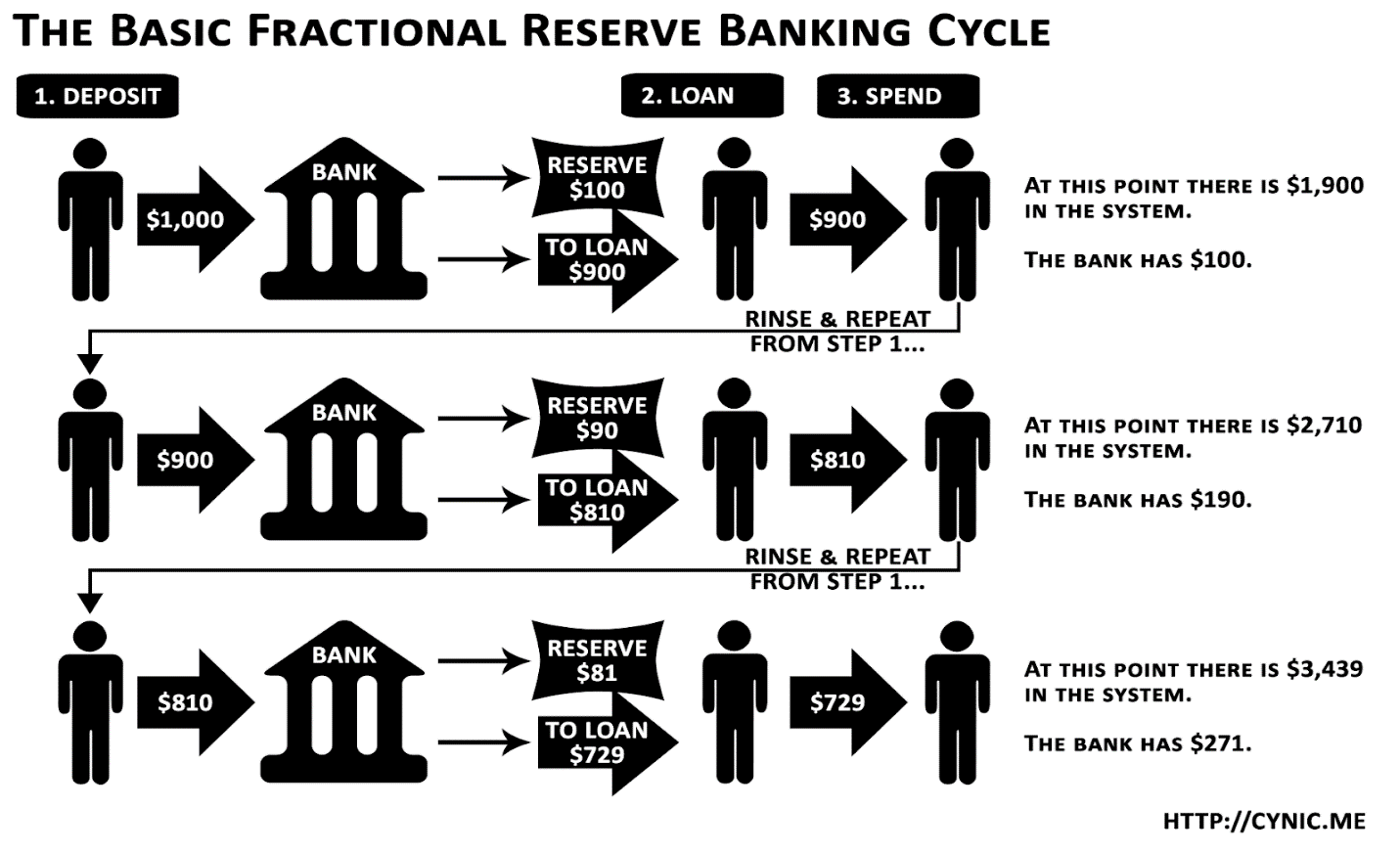

Fractional reserve banking allows banks to increase the money supply without having to “print” a single dollar. Let’s say that you deposit $1,000 in the bank, as shown in the example below. The bank only has to keep 10% of that $1,000 (or $100) in reserve, meaning that they can loan out the other 90% (or $900). This increases the money in the system from $1,000 to $1,900. Your neighbor then takes a $900 loan from the bank. The bank keeps 10% ($90), and then loans out 90% (or $810), thus increasing the money in the system to $2,710. This cycle continues and money seemingly appears out of thin air. This vast increase in US currency through banks and government lending has begun an increase in inflation.

This graphic depicts how banks use fractional reserves to increase the money supply.

Understanding how the money supply increases and subsequently causes inflation is important, but what can be done about it? The most effective way for the government to deter inflation is by raising interest rates. Raising interest rates tends to incentivize Americans to save, thus discouraging borrowing and lending. This also tends to slow economic growth.

In the face of this economic uncertainty, it’s easy to feel anxious. So, what should retirees do?

First, stay informed. There are likely great fixed interest rate opportunities that lie ahead. Fixed interest rates will protect the value of your money should interest rates increase. Second, increase your income. Consider a pension or social security cost-of-living-adjustment (COLA) increase. The purpose of a COLA is to reduce how much inflation affects your retirement income.

[RETIREMENT ACCOUNT WITHDRAWALS?]

All in all, don’t panic. Inflation alone is unlikely to dramatically influence your retirement plan. It’s important to understand how your retirement may be influenced by potential “what ifs?” but the best thing you can do is have a sound plan that can provide you with the peace of mind to get back to what really matters to you. Contact our office today for a complimentary consultation to discuss a retirement plan that works with your individual needs and concerns. While there is chance inflation will affect your retirement, it’s important to remember that the very most likely thing that should happen to you during retirement is that you continue to live life and enjoy every moment of it.